The 2026–27 Australian Defence Portfolio Budget Statement (PBS) confirms a strategic shift that has been building across successive defence reviews, force posture decisions and industrial reforms: Australia is transitioning from a peacetime preparedness model toward sustained strategic competition.

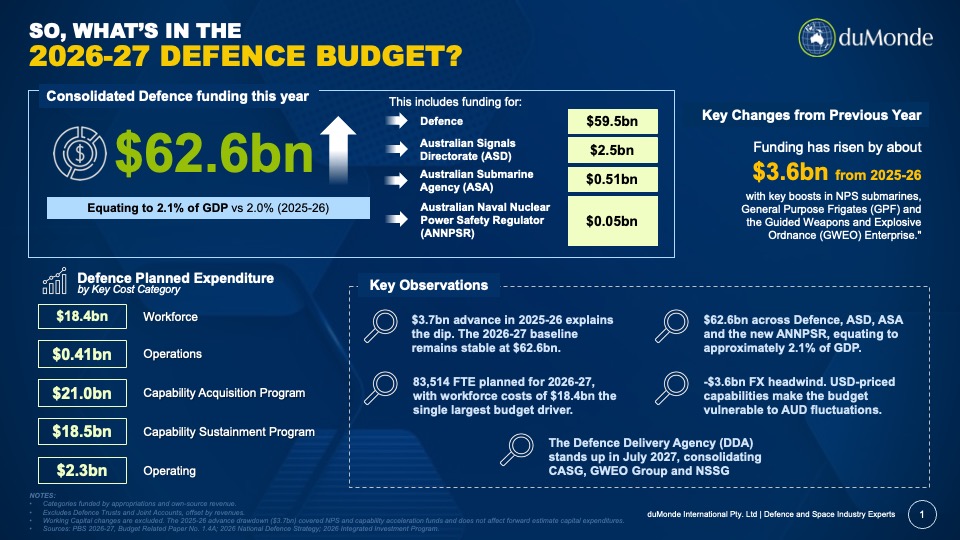

At $62.6 billion in 2026–27 and approximately $340.4 billion across the forward estimates, the Budget operationalises the priorities established in the 2026 National Defence Strategy (NDS) and updated Integrated Investment Program (IIP). Over the decade to 2035–36, the Government’s Defence funding envelope now reaches approximately $887 billion, including around $425 billion in allocated capability investment.

This is more than a larger Defence budget. It is a broad restructuring of Australia’s strategic posture, industrial base and acquisition system.

The strategic assessment underpinning the package is clear: Australia’s operating environment is becoming more contested, less predictable and increasingly compressed in terms of response time. The 2026 NDS reflects a Government judgement that preparation for high-end strategic competition can no longer be treated as a long-term future contingency. For Defence industry, investors and allied partners, the implications are substantial.

Five Strategic Themes Define the Budget

The 2026–27 PBS is built around five mutually reinforcing priorities.

1. AUKUS and Undersea Warfare Become the Apex Investment

The nuclear-powered submarine enterprise now sits unequivocally at the centre of Australian defence planning. Total undersea warfare investment is projected at between $94 billion and $130 billion across the decade, including $71–$96 billion for the nuclear-powered submarine pathway itself.

Importantly, only around $14 billion of this investment is currently approved. The remainder remains contingent on future approvals, industrial readiness, allied coordination and delivery confidence.

The strategic pathway is now clearer:

- Submarine Rotational Force–West (SRF-West) begins from HMAS Stirling as early as 2027

- Australia acquires Virginia-class submarines from the early 2030s

- SSN-AUKUS construction commences at Osborne later this decade, with the first Australian-built boat planned for the early 2040s

However, the defining constraint is no longer funding.

It is workforce. Nuclear-qualified engineers, maintainers, regulators, naval personnel and program managers remain the single most critical bottleneck across the entire AUKUS enterprise. The Budget acknowledges this indirectly through substantial workforce growth measures, but the scale of the challenge remains exceptional.

2. Maritime Power Projection Is Expanding at Scale

The maritime domain absorbs the largest share of the decade-long investment profile.

Australia’s future surface fleet now includes:

- 11 General Purpose Frigates (GPF) based on the upgraded Japanese Mogami-class design

- 6 Hunter-class anti-submarine warfare frigates

- 3 upgraded Hobart-class destroyers

- 6 Large Optionally Crewed Surface Vessels (OCSVs)

The strategic significance of the Mogami-class decision extends well beyond capability.

Japan’s largest-ever defence export deal — valued at approximately USD$6.5 billion — represents both a defence capability decision and a broader strategic-industrial alignment between Canberra and Tokyo. The first three vessels will be constructed in Japan from 2029, with the remaining eight planned for construction at Henderson in Western Australia.

This reinforces Henderson’s emergence as a nationally significant naval construction and sustainment hub alongside Osborne and HMAS Stirling. Collectively, these precincts are evolving beyond traditional Defence facilities into integrated industrial ecosystems supporting continuous shipbuilding, sustainment, workforce generation and long-term sovereign maritime capability.

3. Long-Range Strike and GWEO Reflect Lessons from Modern Conflict

Perhaps the clearest doctrinal shift within the Budget is the acceleration of long-range strike and sovereign munitions manufacturing.

The Government has drawn direct lessons from Ukraine and the Middle East regarding:

- Stockpile depletion rates

- Precision strike relevance

- Industrial resilience

- Supply chain vulnerability

- Autonomous mass and expendability

The resulting investment profile is substantial:

- Targeting and long-range strike: $28–$35 billion

- Guided Weapons and Explosive Ordnance (GWEO): $26–$36 billion

This includes:

- Tomahawk integration

- SM-2 and SM-6 capability expansion

- HIMARS

- LRASM and Joint Strike Missile integration

- Sovereign hypersonic development under AUKUS Pillar II

The key policy signal is unmistakable: Australia no longer intends to rely exclusively on offshore resupply during sustained conflict. Domestic manufacturing capacity is now treated as a strategic capability in its own right.

4. Autonomous Systems Move from Experimentation to Force Structure

The Budget also confirms that autonomous and uncrewed systems are no longer peripheral innovation projects. They are becoming embedded into the future force structure.

Among the most notable developments:

- Ghost Shark XL-AUV progresses under a $1.7 billion contract with Anduril Australia

- Bluebottle expands toward a fleet of 55 sovereign uncrewed surface vessels

- MQ-28A Ghost Bat continues as Australia’s first domestically designed combat aircraft in 50 years

- Counter-UAS capabilities accelerate under LAND 156 and ASCA initiatives

What distinguishes this investment cycle from previous Defence innovation programs is the emphasis on operational relevance and rapid fielding. Ghost Shark’s early prototype delivery — achieved one year ahead of schedule — is particularly important because it demonstrates that accelerated sovereign capability development is possible when acquisition urgency, industrial incentives and operational need align.

5. The Defence Delivery Agency May Be the Most Important Reform of All

While submarines and strike systems dominate headlines, the most consequential long-term reform may ultimately be institutional rather than technological.

The creation of the Defence Delivery Agency (DDA) consolidates CASG, GWEO Group and the Naval Shipbuilding and Sustainment Group into a single delivery structure under a National Armaments Director reporting directly to Ministers.

This is the most significant acquisition reform undertaken in a generation.

The rationale is straightforward:

Australia has historically been more successful at approving ambitious programs than delivering them predictably.

The DDA is therefore an attempt to address systemic acquisition fragmentation, accountability gaps and delivery inefficiencies that have affected Defence programs for decades.

Whether it succeeds will depend less on organisational charts and more on culture, commercial capability, workforce maturity and sustained political discipline. Structural reform alone does not automatically produce delivery performance.

The Real Story Is Not the Headline Number

The most important insight from the 2026–27 Budget may not be the topline funding figure itself.

It is the transition from episodic capability acquisition toward continuous national-scale defence industrial mobilisation.

Three structural realities now shape the Defence environment simultaneously:

- Capability complexity is increasing dramatically

- Sustainment costs are growing faster than acquisition

- Industrial capacity — not policy ambition — is becoming the principal limiting factor

Capability sustainment alone grows to $24.4 billion annually by 2029–30. Nuclear-powered submarines, integrated missile defence, autonomous fleets and advanced strike systems fundamentally alter the long-term operating cost profile of the ADF.

At the same time, Australia is attempting to execute multiple generational-scale programs concurrently:

- Nuclear-powered submarines

- Hunter-class frigates

- General Purpose Frigates

- GWEO manufacturing

- Northern base hardening

- Autonomous systems integration

- Amphibious force restructuring

- Enterprise ICT and AI modernisation

This creates an industrial absorption challenge unprecedented in modern Australian defence history.

The strategic question is no longer whether the Government intends to spend.

The question is whether the national industrial ecosystem can scale quickly enough to absorb, sustain and deliver the program at the required pace.

Workforce and People-Related Capability

One of the clearest signals within the 2026–27 PBS is that Defence capability is now being treated as fundamentally inseparable from workforce capacity.

Workforce costs — covering permanent ADF personnel, APS employees and elements of the external workforce — are forecast at $18.39 billion in 2026–27, increasing to $20.71 billion by 2029–30. This makes workforce expenditure one of the largest structural cost categories in the Defence budget, alongside capability acquisition and sustainment.

The scale of planned growth is substantial.

The Budget funds an average full-time equivalent workforce of 83,514 personnel in 2026–27, comprising:

- 63,345 permanent ADF personnel

- 20,169 APS employees

Reserve capability also remains increasingly important to Defence preparedness and domestic resilience tasks. Current planning assumptions include approximately 1.18 million service days generated from around 23,300 Reservists, supporting operational readiness, regional engagement and domestic response requirements.

Importantly, workforce growth is no longer simply a personnel policy issue — it is now a strategic capability issue.

Across AUKUS, naval shipbuilding, guided weapons manufacturing, cyber, AI-enabled systems, sustainment and acquisition reform, the limiting factor increasingly becomes access to highly specialised labour pools rather than funding availability alone. Nuclear-qualified engineers, program managers, systems integrators, ICT specialists, maintainers and industrial trades represent some of the most constrained cohorts across the entire Defence enterprise. This explains why workforce reform, retention incentives, non-citizen recruitment pathways and industry-government workforce partnerships have become central pillars of the broader National Defence agenda.

Capability Sustainment and Preparedness

While public attention often focuses on new platforms and acquisitions, one of the most consequential long-term dynamics within the Budget is the rapid growth in sustainment expenditure.

Planned expenditure under the Capability Sustainment Program reaches $18.5 billion in 2026–27 and grows to $24.4 billion by 2029–30.

This reflects a structural reality confronting all advanced military forces: as capability sophistication increases, sustainment complexity and cost grow disproportionately.

The ADF is simultaneously operating and modernising:

- high-end maritime combatants

- fifth-generation air combat systems

- integrated missile defence

- advanced ISR networks

- cyber and digital infrastructure

- autonomous and uncrewed systems

- the foundational infrastructure for nuclear-powered submarines

Maintaining operational readiness across that force structure requires sustained investment not only in platforms, but also in logistics, software, maintenance systems, workforce, data infrastructure and industrial support networks.

Key sustainment allocations in 2026–27 include:

- Navy — $3.78 billion

- Army — $2.80 billion

- Air Force — $4.24 billion

- Defence Digital and ICT sustainment — $2.16 billion

- Security and Estate sustainment — $3.74 billion

- Joint Capabilities — $0.96 billion

- Defence Intelligence — $0.30 billion

- Nuclear-Powered Submarines sustainment — $0.07 billion

- Guided Weapons & Explosive Ordnance sustainment — $0.20 billion

The strategic implication is significant. Australia’s future Defence capability edge will depend not only on acquiring advanced systems, but on sustaining them at readiness over prolonged periods of strategic competition. The sustainment enterprise is therefore becoming a core component of deterrence itself.

Capability Acquisition and Infrastructure

The Capability Acquisition Program remains the primary engine of Defence modernisation.

Planned expenditure reaches $21.0 billion in 2026–27 and is projected to increase to $27.1 billion by 2029–30.

This funding supports the acquisition of major military platforms, enabling infrastructure, ICT modernisation and broader Defence estate expansion required to support the future integrated force.

Within the 2026–27 allocation:

- approximately $15.4 billion is directed toward military equipment acquisition

- around $4.25 billion supports estate and infrastructure investment

- approximately $0.82 billion is allocated to ICT acquisition

The breadth of this investment profile highlights an important strategic shift.

Defence capability is no longer being conceptualised solely through major platforms such as ships, aircraft or armoured vehicles. Increasingly, the enabling ecosystem — secure ICT architecture, hardened infrastructure, logistics networks, fuel resilience, northern basing, cyber resilience and digital integration — is being treated as equally critical to operational effectiveness. This is particularly evident in the substantial investment directed toward northern bases, naval shipbuilding precincts, submarine infrastructure, Defence estate modernisation and enterprise digital transformation. Together, these projects reflect a broader transition from platform-centric procurement toward integrated national defence infrastructure development.

What Industry Should Take From This

For Defence industry, the PBS represents the strongest and most sustained demand signal Australia has ever produced.

But the environment is changing in important ways.

Government expectations are shifting from transactional procurement toward sovereign capability partnership.

Industry participants will increasingly be assessed not only on cost competitiveness, but also on:

- Workforce development capacity

- Sovereign manufacturing contribution

- Supply chain resilience

- Data and cyber maturity

- Sustainment capability

- Export relevance

- Scalability under crisis conditions

Five sectors appear particularly well positioned over the coming decade:

- Nuclear-powered submarine supply chains

- Guided weapons and domestic munitions manufacturing

- Autonomous and uncrewed systems

- Naval sustainment and shipbuilding workforce services

- Defence ICT, AI and secure data infrastructure

The forthcoming Defence Industry Development Strategy will likely sharpen these expectations further — particularly around workforce scalability, sovereign supply chain maturity, industrial resilience and delivery readiness. For industry, the opportunity environment is genuine, but so too are the expectations. The organisations best positioned over the next decade will be those capable not only of winning work, but of delivering at scale, sustaining capability over time and integrating effectively into a national defence industrial mobilisation effort.

Final Assessment

The 2026–27 Defence Portfolio Budget is strategically coherent, financially substantial and institutionally ambitious.

It reflects a Government that has concluded Australia’s strategic environment has entered a fundamentally more dangerous phase — and that deterrence now requires not merely modernisation, but sustained national mobilisation capacity.

The Budget’s greatest strength is its integration.

The NDS, IIP and PBS are no longer operating as separate policy artefacts. Together, they now form a coordinated strategic framework linking capability, industry, workforce, infrastructure and acquisition reform into a single long-term national defence program.

The challenge ahead is execution.

Funding trajectories can be announced quickly. Building nuclear workforces, sovereign industrial ecosystems, resilient supply chains and acquisition cultures capable of delivering at scale is considerably harder. The next decade will determine whether Australia’s defence transformation becomes a successful strategic realignment — or a cautionary example of ambition outpacing national capacity.

duMonde Summary and Analysis of the 2026-27 Australian Defence Portfolio Budget

Access the full report